[ad_1]

DEC CORN

The Dec Corn chart above is a perfect microcosm of the CBOT commodities – a supply Bull facing off a Demand Bear – resulting in a tight congestion pattern – a range-bound (670-700) since Labor Day! The bullish feature of course is the short 2022 crop – pegged at 10% under last year – with beginning stocks already on 6-7 year lows! The bearish feature is the paltry exports of late – due to a non-competitive US price, a sluggish China economy and transportation issues on the historically low Mississippi River! The Ukraine Grain Corridor is on-again/off-again! The Macros have been very supportive – with DJI rallying 3000 points & the US $$ dropping 400 points on the perception the Fed will take their “foot off the gas”! The S/A crop is reputed to be record large – but anything less could well rally the mkt!!

NOV BEANS

Nov Beans, likewise, are caught in a tight trading range (1350-1410) since Oct 1 – albeit $1.00 over its recent highs – unlike Dec Corn – which is snugging right up to its recent highs! The difference is the 800 pound Gorilla in the room – a forecast record bean crop in Brazil the worlds’ largest producer! The US harvest is 80% done & probably 95% next week – so the mkt focus will shift to South America’s crop & the weekly weather during its planting! The plummeting US Dollar has been a major supporter of the mkt on breaks – as it falls off from 20 year highs – on the feeling the Fed will ease off IR increases in early 2023! Once US Bean prices become more competitive & China’s economy recovers from its zero-Covid policy, bean exports should pick up! There are early indications of that as the Monday Inspections were nearly 3 MMT! Should the US $ continue to free-fall, The Ukraine Corridor Deal fall apart & The S/A bean crop, disappoint, Bean futures will get a solid upside bolt!

DEC WHT

The chart patterns are bearish! And validating that was Dec Wht’s inability to rally yesterday after a sharp drop in the US Dollar! Winter Wht planting is 79% in (avg-78). The mkt needs a production shortfall somewhere or an export increase to turn it around! Australia is having some rain issues & should the Ukraine Grain Corridor Pact not be renewed in late November, wht futures will soar! Stay tuned!!

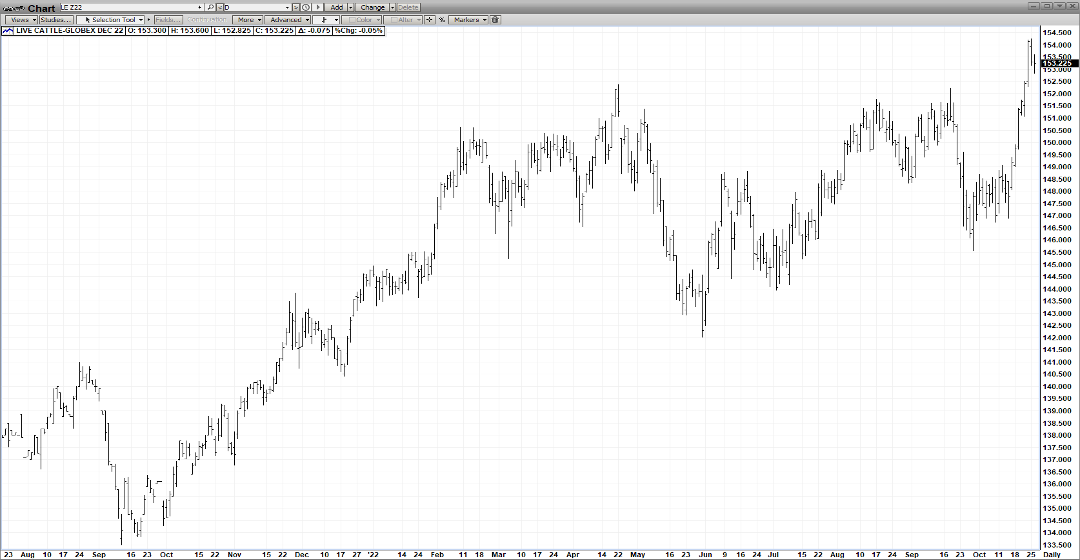

DEC CAT

Yesterday, Dec Cat posted new contract highs before key-reversing from an overbought position to close lower! Probably just a correction given the strong cash & boxed beef mkts! The supply/demand fundamentals are quite strong! Production in each of the next four quarters is forecast to drop 3-8%! YTD exports are up 11%! Feed cost for meal & corn are quite high! And most importantly, demand has been stellar – as the consumer – despite looming recession fears, continues to cut back on everything but food!

DEC HOGS

The improbable, nearly vertical $17 rally (73-90) in Dec Hogs since Oct 4 may correct very soon from its overbought condition as slaughter is likely to increase in the weeks ahead & the USDA pork cut-out came in at 97.07 – down $3.34 from Monday & its lowest level since Sept 30! Still, the upsurge – mostly sans China imports – is remarkable & is a testament to the domestic demand – which despite a looming recession – remains stalwart!!

Questions? Ask Bill Moore today at 312-264-4337

[ad_2]

Image and article originally from blog.pricegroup.com. Read the original article here.