[ad_1]

Vital Statistics:

| Last | Change | |

| S&P futures | 3,952 | 12.50 |

| Oil (WTI) | 76.35 | 1.24 |

| 10 year government bond yield | 3.58% | |

| 30 year fixed rate mortgage | 6.28% |

Stocks are higher this morning on no real news. Bonds and MBS are up small.

Jerome Powell spoke yesterday and it doesn’t appear that he had much to say in terms of current monetary policy. The issue at hand was central bank independence. Powell acknowledged that rate hikes will be unpopular politically, but welcomed the absence of political control over monetary policy. I suspect this is temporary, and if the economy slows dramatically the Fed will see pressure from Congress to cut rates.

Powell also acknowledged that the Fed is getting pressure to “act on climate.” This means he is getting pressure from activists to use the Fed’s supervisory authority to discourage investment in fossil fuels. Climate Action 100 is a consortium of banks and investment firms that have pledged not to lend to energy companies, and I suspect the activists want the Fed to either explicitly prohibit fossil fuel lending or to use some other lever to discourage it. Powell pushed back on this: “But without explicit congressional legislation, it would be inappropriate for us to use our monetary policy or supervisory tools to promote a greener economy or to achieve other climate-based goals. We are not, and will not be, a “climate policymaker.”

Mortgage Applications fell 1.2% last week as purchases fell 1% and refis fell 5%. Total applications are down 48% on a YOY basis and refis are down a whopping 86%. “Mortgage rates declined last week as markets reacted to data showing a weakening economy and slowing wage growth. All loan types in the survey saw a decline in rates, with the 30-year fixed rate falling to 6.42 percent. Purchase applications continued to be hampered by broader weakness in the housing market and declined slightly over the week, with the index slipping to its lowest level since 2014,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “There was an increase in refinance activity as a result of the 16-basis-point decline in rates, as both conventional and government refinance applications increased. However, the overall pace of refinance applications was lower than November and December’s 2022 averages, and over 80 percent lower than a year ago. Refinances were about 30 percent of all applications last week — well below the past decade’s average of 58 percent.”

Wells is drastically shrinking its mortgage footprint. It will exit correspondent and will only originate mortgages for its own clients and borrowers in minority communities. Not too long ago, Wells was the biggest mortgage banker in the US. “We are acutely aware of Wells Fargo’s history since 2016 and the work we need to do to restore public confidence,” [Chief Consumer Lending Officer] Santos said in a phone interview. “As part of that review, we determined that our home-lending business was too large, both in terms of overall size and its scope.”

Wells will also be significantly shrinking its servicing portfolio. It is amazing how much capacity is being wrung out of the mortgage business over the past year. This should translate into higher margins into 2023.

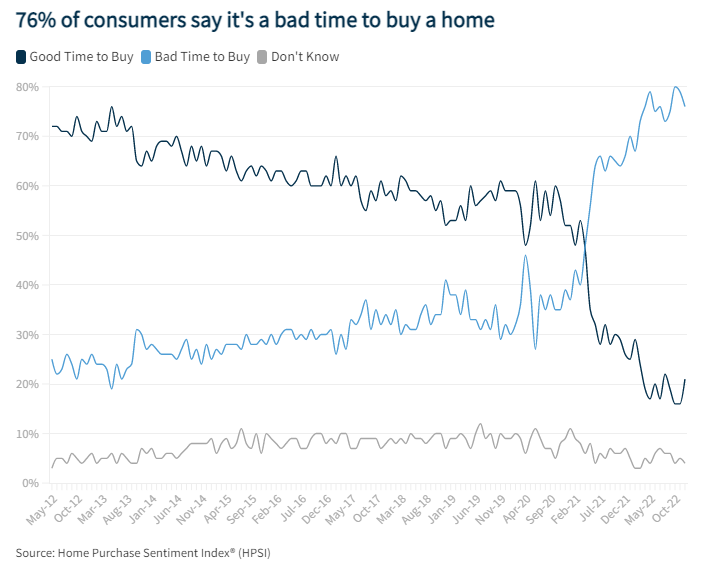

Are we seeing signs of a turn in housing? Perhaps. The Fannie Mae Home Purchase Sentiment Index increased in December, albeit it is barely higher than the all-time low set in October. “In December, the HPSI inched upward slightly, as consumers reported increased expectations that mortgage rates and home prices may decrease over the next year – perhaps reflecting recently observed declines in mortgage rates and average home prices,” said Doug Duncan, Fannie Mae Senior Vice President and Chief Economist. “However, the HPSI remains very low by historical standards, particularly the ‘good time to buy’ component, and respondents continue to cite high home prices and unfavorable mortgage rates as the primary reasons for their pessimism. As we enter 2023, we expect affordability to remain the top challenge for potential homebuyers, as even small declines in rates and home prices – from the perspective of the buyer – may not produce sufficient purchasing power. At the same time, existing homeowners may continue to wait to list their properties, since many have already locked in lower mortgage rates, creating minimal incentive to sell and buy again until rates are more favorable. We think the resulting tension will contribute to a continued decline in home sales in the coming months.”

I launched my Substack over the weekend, where I took went over the market’s reaction to the jobs report and the main drivers. The Weekly Tearsheet will take a deeper dive into some of the happenings in the prior week, along with economic commentary. I hope you enjoy it and consider subscribing. If you use this professionally and can expense it, I hope you consider becoming a paid subscriber.

I am accepting ads for this blog as well, if you would like a mention. In addition, if you enjoy the content and would like a white label solution for your company, I would be interested in having a conversation.

[ad_2]

Image and article originally from thedailytearsheet.com. Read the original article here.